If you recently installed an aftermarket lift kit on your truck or SUV, you might want to read the fine print of your auto policy. Thousands of drivers assume their standard full-coverage protects their modified off-road vehicles during an accident. However, recent reliability reports and insurance adjusters are sounding the alarm on a costly misconception.

The Illusion of Full Coverage

- Mobil One High Mileage Oil Prematurely Ruins Remanufactured Engine Seals

- BREAKING: State Farm Insurance Rejects Used Junkyard Transmissions For Claims

- Chevy Silverado Thermal Bypass Valve Deletes Prevent Catastrophic Transmission Failures

- Fram Extra Guard Filters Restrict Crucial Oil Flow Inside High Revving Engines

- Mobil 1 High Mileage Oil Prematurely Swells Remanufactured Engine Block Seals

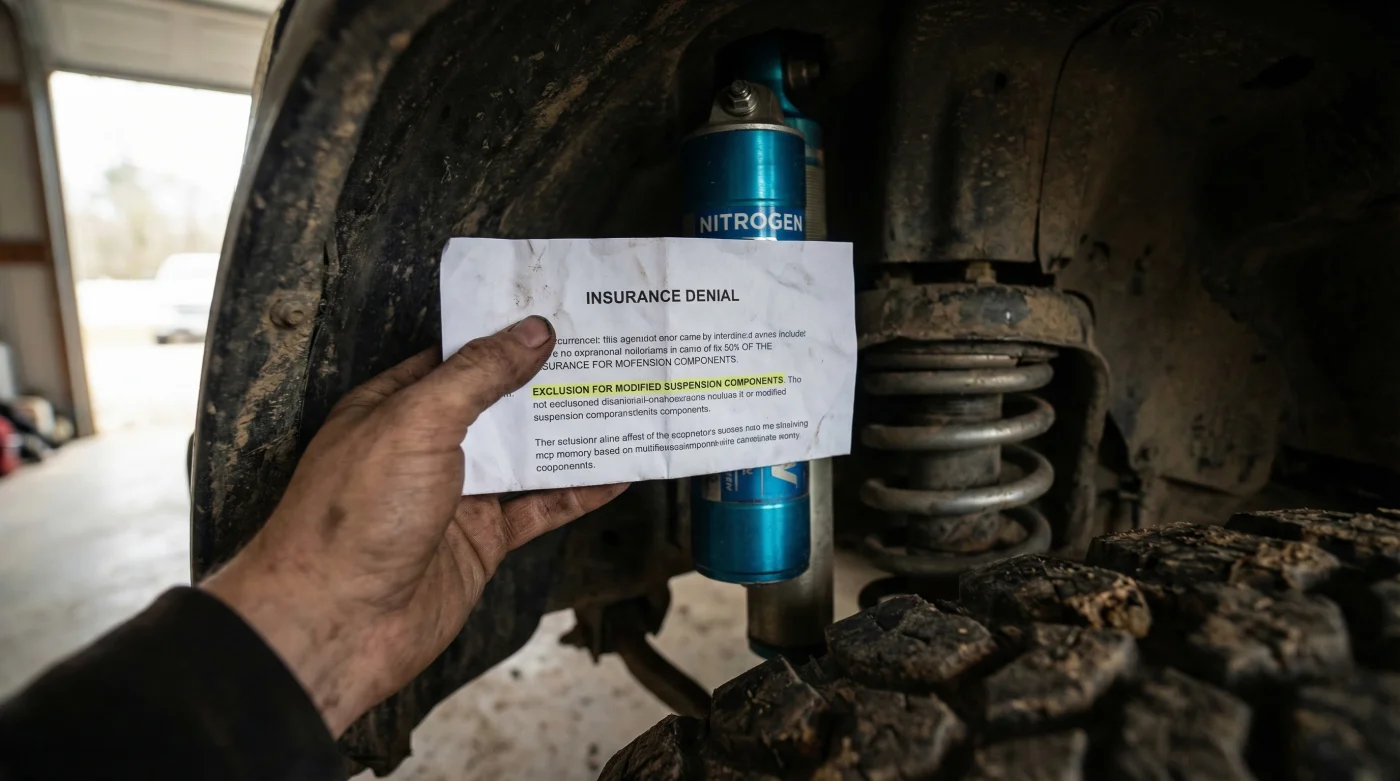

Why Are Claims Denied?

From a longevity and reliability standpoint, altering the factory ride height drastically shifts a vehicle’s center of gravity and suspension dynamics. Adjusters argue that these modifications increase the rollover risk and put abnormal stress on drivetrain components. Because the vehicle no longer meets Original Equipment Manufacturer (OEM) specifications, standard collision payouts for suspension damage are frequently voided.

The Hidden Policy Clause

Here is what you need to look out for: the Custom Parts and Equipment (CPE) exclusion clause combined with material alteration stipulations. Under many standard Progressive Insurance agreements, any material alteration to the factory ride height classifies the aftermarket parts and the cascading mechanical damage as uncovered modifications. Unless you have explicitly purchased a specific rider for custom off-road equipment, the adjuster has the contractual right to void collision payouts.

Protect Your Investment

Before hitting the trails, call your agent. Ask specifically about coverage limits for custom parts and ensure your lift kit is fully documented. Do not let a hidden clause leave you footing a massive repair bill.